TL20 leads benchmarks

Year-to-date, the TL20 group of stocks to consider is up twenty-four percent, better than the three-percent gain of the Nasdaq and the two-percent gain of the S&P 500. Read about the TL20

WHY I CREATED TL

Limited-time offer for new subscribers: $1 a week for four weeks

Shares of chip equipment giant ASML are down five percent Wednesday at $1,437.18 for the Nasdaq-listed American Depository Receipts, mainly reacting to a lower-than-expected sales outlook for this quarter (but an increased outlook for the full year 2026.)

What adds a little salt to the wounds today is that this is the first quarter that the company ceased reporting the number of orders it received for equipment, something they warned us a year ago they would do..

The argument a year ago from ASML’s CEO, Christophe Fouquet, and CFO, Roger Dassen, was that order rates can be volatile, quarter to quarter, so, it’s best not to obsess over them quarter to quarter. But, when a given quarter’s forecast doesn’t totally delight, as this one didn’t, order data would have been a little bit of a comfort. And, to add even more salt, the January report, the last quarter in which they did disclose, had been a blow-out report at the time, with order numbers coming in way above expectations

Shares of Bloom Energy, makers alternative energy products in the form of a solid-oxide fuel cells used to power data centers, soared 24% on Tuesday to close at $219.03, after the company late Monday announced an expansion of its relationship with Oracle as a customer, which prompted at least one bear on the stock to ease up on his negative view.

The Oracle deal has the potential to deliver 20% to 50% upside to the Street’s revenue estimates, writes Jefferies & Co. analyst Dushyant Ailani, who raised his rating on Bloom shares Tuesday to Hold from Underperform, with a $187 price target, up from $97.

Ailani is “nearly on the bandwagon” with the stock, he writes, but what is holding him back is valuation. “We view valuation as stretched,” he writes, adding, “Bloom epitomizes retails infatuation with 'new' technology and data centers with the valuation divorced from fundamentals.”

One of the newer chapters of the frantic artificial intelligence trade has been the positive view on the operators of so-called content distribution networks, or, CDNs, principally Fastly and Akamai. Those stocks were two of the only bright spots in software and services, rising as much as 229% through early April in Fastly’s case, and 37% in Akamai’s case.

Last week those gains began to unravel fast as investors realized they blew the notion of AI “agents” out of proportion.

The bullish argument in favor of Fastly and Akamai and others such as Cloudflare, and privately held Vercel, is that lots of AI programs in the form of agents would run around the enterprise, creating a surge in traffic across networks, which would be a direct boost to the companies selling the ability to manage network bandwidth.

There is a scarcity of advanced chip-manufacturing capacity, notes Northland Securities’s Gus Richard on Monday, raising his price target on Intel shares to $92 from $54. That would represent a return of about forty percent from Monday’s close of $65.18.

Richard reiterates an outperform rating on Intel stock.

Richard emphasizes that there just isn’t that much sophisticated manufacturing capacity extant, and so he believes Intel should trade at three times the value of its manufacturing property, plant and equipment (PP&E).

“Intel now has 3 fabs capable of 3nm and below,” he notes.

“3nm capacity is expected to tighten in CY27, increasing the value of 3nm fabs.”

Richard notes Intel has come a long way:

Rumors are swirling that Nvidia could be considering buying Dell or HP or another PC-related company following a report Monday by Charlie Demerjian of the tech blog SemiAccurate.

Dell closed up 7% and HP shares closed up 5% Monday. Nvidia shares rose fractionally.

Citing what he says has been a year of his own research, Demerjian writes, “Nvidia is looking to make a huge purchase that will reshape the PC and server landscape like nothing else has done since the computer was invented. And let us say again, we are dead serious here.”

I don’t have any information beyond Demerjian’s speculation — and I give him the benefit of the doubt that he’s come up with real signals, real chatter, what have you.

My interest is in Nvidia’s enviable profit versus the PC makers. Nvidia’s gross profit margin at the moment is about 75%. Dell’s margin is 19%, and HP’s is similar.

Solid-state drive maker SanDIsk has been an amazing performer, its shares up 301% this year, and almost 3,000% since it spun out of Western Digital last year, at a recent $952.50.

As SanDisk stock keeps rising, there’s quite a bit of anxiety that the very healthy market for NAND-flash-based drives is bound to cool off, as prices have become a deterrent to further consumption.

NAND, and NAND-based devices such as solid-state drives, are traditionally a commodity, and that has traditionally lead to vicious cycles: sharp swings in the market, driving up prices and margins only to drive them down sharply again.

On Monday, Amit Daryanani agues things are different. The market is still cyclical, but profit will hold up better for SanDisk this time because the company is “structurally” more profitable. He starts the stock at Outperform with a $1,200 price target. That’s based on 12 times what he projects as $100 per share in earnings in the fiscal year ending June of 2027. (He’s slightly higher than consensus for about $99.)

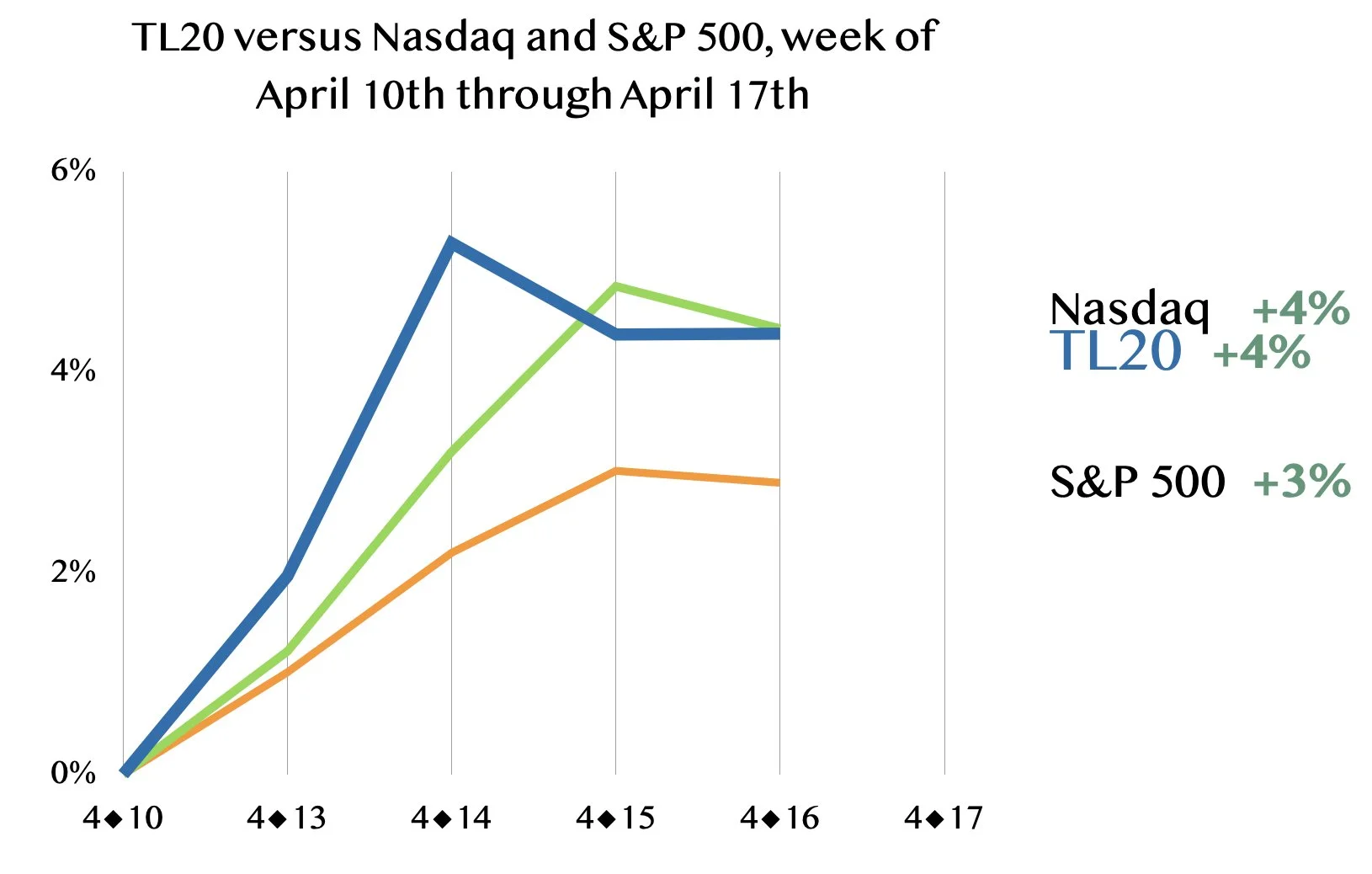

The week that ended April 10th, 2026, was a solid one for stocks as the “AI trade” was reinvigorated by the PR stunt of startup Anthropic, even as plain-old software names Nutanix and ServiceNow got downgraded.

Shares of the TL20 group of stocks to consider soared a collective 12% for the week, lead by shares of Broadcom, Micron Technology, ASML and SanDisk, up 18%, 11%, 13% and 18%, respectively. The only thing doing really poorly in AI last week was Palantir, down 13% and now down 28% year-to-date.

The Nasdaq Composite Index was up 5% and the Standard & Poor’s 500 Index, up 4%.

Anthropic said its “Mythos” AI model is so powerful it will not release it generally to the public but instead share the model with a select group of firms including Google, Nvidia and Cisco. It will do so in conjunction with a cyber-security framework it calls Glasswing.

You would think one of the areas of software most vulnerable to being dis-intermediated by artificial intelligence would be that of “observability,” also sometimes called “DevOps.”

That is software that monitors programs running inside companies to make sure they’re performing right. Those tools, of which Dynatrace and Datadog are the main providers, could conceivably be replaced some day by the kinds of automation emerging every single week from the AI giants, such as the “Glasswing” software that Anthropic promoted this week.

Every time those companies show their resilience, such as Datadog’s earnings report in February, their stocks sell off anyway. Datadog stock is down almost 20% this year, and up 17% in twelve months, vastly trailing the Nasdaq. Dynatrace has been even worse, down 22% this year and the same amount over the past twelve months.

But, the DevOps stuff will prove more resilient than expected, writes Howard Ma of Guggenheim Securities, who on Thursday raised his rating on Datadog to a Buy from Neutral, after concluding that there is plenty of stuff that AI won’t be able to do on its own.

It’s not every day that a bunch of incredibly powerful companies that are in bed together stage a PR stunt, but it does seem like it’s happening more and more.

This week, AI startup Anthropic, which is valued at $380 billion as of its latest $30 billion round of funding, announced that it a) has a new kind of AI large language model in the works, called “Mythos,” and b) that it is not releasing Mythos to the public because it’s too powerful, but that it will instead provide the model to various parties that are cooperating to address thousands of flaws that Mythos found in software.

The cyber-security effort is called Project Glasswing, and, surprise, it brings together mostly Anthropic investors. Project participants including Alphabet’s Google, Microsoft, Nvidia, Amazon, Cisco Systems, and JPMorgan Chase, all of which have put money into Anthropic, according to FactSet Systems.

In addition, Broadcom is part of the effort. As I mentioned Tuesday, Broadcom is selling racks of Google’s “TPU” AI chips to Anthropic, making both Broadcom and Google vendors to Anthropic with a financial interest.

“Did the agent double-check all the things that might be wrong? Did it make assumptions, and, inasmuch as you could even say that it's making an assumption, did it get confused somehow?”

Shares of Broadcom are up almost six percent Tuesday at $332.77 after the company announced in a federal filing after market close on Monday that it inked an agreement with Alphabet’s Google to supply the company with Google’s “Tensor Processing Unit,” or, TPU, its custom AI chip, and related technology through 2031.

Broadcom and Google have collaborated for years to produce the TPU, which Google designs and Broadcom then helps to shepherd through the manufacturing process with Taiwan Semiconductor Manufacturing. So, this is an extension of an existing arrangement.

In the same filing, Broadcom confirmed a deal first announced in December with AI startup Anthropic, saying it will supply 3.5 gigawatts of computing capacity to Anthropic, in the form of complete rack systems using the TPU, through 2027.

The week that ended April 3rd, interrupted on Friday by the Good Friday markets holiday in the U.S., saw stocks surge, with the Nasdaq Composite Index up 4%, the Standard & Poor’s 500 up 3%, and the TL20 group of stocks to consider up 6%, with most names seeing net gains for the week.

The headlines were dominated by continued debates over the memory-chip trade concerning Micron Technology, SanDisk, and Seagate, by new worries for ASML and chip-equipment makers with respect to China, and by the announcement of an unprecedented $122 billion private round of funding for OpenAI.

The memory-chip debate continues as the Street wonders how long extraordinarily high profit margin can continue for Micron from surging DRAM and NAND prices. I covered this a bit last week, the worries over “spot pricing.”

Oracle’s bizarre transformation from a software titan to an industrial company gained a new component on Monday as the company announced it has appointed Hilary Maxson, CFO of industrial giant Schneider Electric for six years, as its new CFO, replacing current CFO Doug Kehring immediately.

Oracle stock is down fractionally at $145.57 on Monday, but the analysts covering the company seem pretty pleased. They have to reckon, however, with what I think a proper stock valuation is for Oracle, which I would argue is much less than the current valuation.

In the press release announcing Maxson, Oracle lauds her role at Schneider transforming the company “from an electrical equipment supplier into a digital energy technology partner for key segments, like utilities and datacenters.” Prior to Schneider, Maxson was an executive for a dozen years at American utility AES. (Kehring is staying on at Oracle as head of operations.)

The week that ended March 27th saw the TL20 group of stocks to consider lose all of its gains, and last week, the abbreviated week ending with the Good Friday holiday, saw all that come rocketing back.

The TL20 is up now six percent for the year, vastly outperforming the major indices, which remain in negative territory. Most names rose last week, as you can see in the table below.

The artificial intelligence trade has been dominated by wild amounts of money being spoken of, including more than a trillion dollars that OpenAI has committed to spending on Nvidia GPU chips and other infrastructure. I believe all that money talk is about to come to its denouement, and not in a good way.

OpenAI on Wednesday announced its latest investment round, $122 billion in funding lead by returning investors Nvidia, Amazon, and SoftBank Group, along with a gaggle of other investors including the venture firm a16z (Marc Andreessen and team.)

The round values OpenAI at $852 billion, the company said. That allows us to put a price on all the spending the company has pledged and what it may amount to. OpenAI noted that its revenue is coming in at $2 billion a month, implying revenue this year will reach or exceed $24 billion.

One of the more unusual arguments in favor of Microsoft stock that I’ve seen in a while is contained in the report Wednesday by Yi Fu Lee of The Benchmark Company, who initiated coverage on the shares with a Buy rating and a $450 price target, which would be a 26% gain from the closing price of 369.37. (The shares sold off slightly on Wednesday.)

Lee values Microsoft at 8.8 times fiscal 2027’s likely revenue, a modest multiple for a powerful software outfit.

Lee’s argument is that investors have ignored the value of all the data of Microsoft customers contained in the many applications that the company sells, including the Office 365 productivity suite, the Dynamics back-office software, and LinkedIn.

There continues to be in the popular imagination a seriously misleading presumption about quantum computing, which is that we will build quantum computers very soon that are hugely powerful.

As I’ve written at length, quantum has a “scaling” challenge: no lab or company has demonstrated that they can reliably build computers with the hundreds of thousands of quantum “gates” necessary to do real work.

Because the public keeps missing that obvious fact, we’re getting doomsday articles such as the piece in Barron’s this week by Mackenzie Tatananni that claims that Google has just told the world that conventional data encryption will be cracked by 2029, years earlier than previously expected.

Shares of chip maker Marvell Technology were soaring thirteen percent on Tuesday to $99.19 as it became the latest beneficiary of Nvidia’s largesse, the two announcing they will work on “silicon photonics” together — the integration of data communications into the processor itself — and that Nvidia will take a $2 billion stake in Marvell (three percent of Marvell’s $77 billion market cap.)

The deal follows investments in Intel last year — almost five percent of the stock — and Coreweave, of which it owns almost thirteen percent, according to 13-F filings compiled by FactSet Systems.

Nvidia’s public equity spending soared in 2025 from almost nothing in all the years prior. According to the 10-K filing for the year, out of a total of $63 billion of cash and equivalents on the books at the end of the January quarter, Nvidia’s investments in marketable securities, which totaled $52 billion, included $12.9 billion in equities (the rest being money markets and debt). That is up from just $381 million a year earlier.

Shares of conglomerate Innventure are up ten percent Tuesday morning at $3.90, after CEO Bill Haskell told analysts on the company’s earnings call Monday evening that his stock is priced too low relative to its assets.

Innventure is majority owner of Accelsius, a startup making “two-phase” liquid-cooling technology for data centers. That company is valued at $665 million, based on outside investments by industrial giant Johnson Controls and French building infrastructure giant Legrand. Innventure stock is currently trading for just $296 million, based on 82 million shares outstanding.

“We're not gonna complain about the market,” said Haskell, “but we are going to state facts. The facts suggest there is a significant gap between where our shares trade and what this platform is worth.”

Shares of conglomerate Innventure are up ten percent Tuesday morning at $3.90, after CEO Bill Haskell told analysts on the company’s earnings call Monday evening that his stock is priced too low relative to its assets.

Innventure is majority owner of Accelsius, a startup making “two-phase” liquid-cooling technology for data centers. That company is valued at $665 million, based on outside investments by industrial giant Johnson Controls and French building infrastructure giant Legrand. Innventure stock is currently trading for just $296 million, based on 82 million shares outstanding.

“We're not gonna complain about the market,” said Haskell, “but we are going to state facts. The facts suggest there is a significant gap between where our shares trade and what this platform is worth.”

The week that ended March 27th brought the biggest challenge to the group of the TL20 group of stocks to consider since the beginning of the year, pushing the TL20 down 4%, erasing all gains for the year.

At least the TL20 is still in better shape than the 10% decline of the Nasdaq since the start of the year, and the 7% decline of the Standard & Poor’s 500.

My post about the TL20 Sunday goes through the names with some comments about how they’re doing.

Not all are negative. Amphenol and Analog Devices are holding up relatively well, with little news flow since their last earnings reports.

The TL20 group of stocks to consider on Friday hit its lowest level since December 31st, elegantly erasing the year’s gains. The stock suffered worse than the Nasdaq Composite Index and the S&P 500 this week, with the 5.5% drop on Thursday being the group’s fifteenth-worst single-day decline. A summary of where they’re at.

Analysts at Jefferies & Co. on. Wednesday published one of the strangest reports I’ve read in a long time, which laid out the case that we are at an “inflection point” for humanoid robots, but actually managed to convince me we are nowhere close to such an event.

The title is cute: “From Aasimov to the Assembly Line, Humanoid Robots Begin to Clock In.”

Except that, they aren’t really. “Atlas is not expected to approach a meaningful cumulative volume of 30,000 units until close to 2030 with Hyundai,” the report notes of Boston Robotics’s flagship unit, Atlas. Tesla’s “Optimus rollout is likely to be dominated by internal use in its factories, given constraints such as harmonic reducer torque density and ongoing mechanical redesign,” they note.

The bulk of the report, which was put together by a whole team of Jefferies analysts, including semi analyst Blayne Curtis and colleagues from all different areas of equities, is filled with rich technical details that are thoughtful.

However, the top-level perspective that has been thrown onto the thing strains to convince you of some imminent financial development that will be useful to a trader or possibly an investor. It is tremendous “organ music,” as in the opening fugue of a great drama.

“Humanity appears to be on the precipice of wider adoption of humanoid automatons,” it boldly states. “Humanoid robots—machines structurally resembling humans and built to operate in environments designed for people—are transitioning from longstanding aspiration to commercial reality.”

Except that the 46-page piece itself, though, is like the fine-print disclaimer about what doesn’t yet work regarding human-like robots.

Morgan Stanley chip analyst Joseph Moore engages in a spirited defense of memory-chip stocks Micron Technology and SanDisk on Thursday, after a sharp drop in their shares this week.

We are not in normal times as his main message, as things that would mark a normal “cyclical peak” in their businesses are moot with the rise of “agentic AI” and the need for much, much more memory.

“Looking for sell signals from prior cycles misses the point,” writes Moore. “Memory is not just constrained by AI demand — memory is increasingly THE primary constraint on AI demand.”

Moore has an Overweight rating on Micron shares, and a $520 price target — almost 50% upside from a recent $357 — and also Overweight on SanDisk stock with a $690 price target, about 13% from today’s $611.

I think Moore is right on the money on all points. Both Micron and SanDisk are in the TL20 group of stocks to consider, and I see good times continuing for both, as I wrote at the beginning of the year.

Both stocks are down sharply today despite his endorsement.

Moore outlines his sense of the factors weighing on shares:

Shares of ARM Holdings are up nineteen percent on Wednesday at $159.99 after the company said Tuesday that it will go into competition for the first time ever with its customers, making its own microprocessor for the data centers, the “AGI CPU.”

At an event at the Fort Mason Center in San Francisco, ARM CEO Rene Haas talked with analysts about the virtues of the AGI CPU to relieve the exhausted x86 CPUs of Intel and AMD. (Interestingly, both AMD and Intel shares surged 7% on the news — we’ll come back to that.)

The question now becomes, having earned the most expensive stock multiple of all semiconductor stocks based on a business of one-hundred-percent profit, or nearly, should ARM stock still trade for twenty-four times next year’s sales as it transitions to a business with fifty-percent profit margin?

Probably not, but let’s go through the numbers.

Merrill Lynch software analyst Tal Liani on Tuesday initiated coverage of CoreWeave, the debt-laden operator of artificial intelligence clouds that is under contract to OpenAI and Microsoft and Meta. It was one of the more interesting initiations in a while because it is positive, with a Buy rating, and a $100 target, but behind the lines, the subtext is quite negative to my mind.

Liani doesn’t write it, but I think the conclusion is that at some point, CoreWeave becomes just a software vendor, shedding the money-losing data center operations.

Liani’s critique boils down to three questions that he calls the “central debates” of investors: 1) Will the company lose its edge as Microsoft and the others build their own AI data centers, and as the game shifts from AI “training,” the making of new AI models, to “inference,” the making of predictions for the masses; 2) are they going to be able to transition to a broader market after having worked for a captive handful of customers for years; and 3) will they be able to keep financing operations that depend on quickly rushing equipment into service in order to pay their enormous debt service.

Deutsche Bank semiconductor analyst Ross Seymore this morning offered up a “chart book” of where semiconductor valuations sit. He notes that the chip equipment companies, including KLA and Lam Research, are the most expensive group: their forward price-to-earnings multiple is well above what the median had been for their stocks.

By contrast, Nvidia and Advanced Micro Devices are well below their median. Seymore sees the disparity between processor companies like Nvidia and equipment companies like Lam to be “puzzling dislocations in relative valuation.”

Seymore offers a handy chart that shows which stocks are expensive and which are cheap based on where their P/E is now relative to the historical median:

I wrote a week ago or so that software stocks are trading below their average price-to-sales multiple and could be acquisition bait.

That has not prevented software from continuing to trade lower in price and lower in reputation.

The latest casualties on Monday are nine software stocks that Jason Ader of William Blair cut from either Buy or Hold to either hold or Sell after concluding that, as he puts it, “AI has injected unprecedented uncertainty into the software sector — every company will need to rethink their product, their pricing, and their GTM strategy.”

I’ve laid out the nine for you in a handy table:

It might seem pointless to be worrying about stock allocations with a war in the Middle East, but my philosophy tends to be in good times and bad, one needs to focus on the quality of stock investment — if you're going to be putting money into the market at all.

Last week, for the seventh rebalancing of the TL20group of stocks to consider, I swapped out five names and swapped in five new ones.

Based on a reference date of March 13th, the TL20 is down a third of a percent in the past week, holding up better than a two-percent fall in the broader indices.

Year to date, the TL20 is up 5%, better than down 7% for the Nasdaq Composite, and down 5% for the S&P 500.

Since inception, the TL20 is up 309%, more than triple the Nasdaq and more than quadruple the S&P.

It has also done much better than benchmarks such as Cathie Wood’s ARK Innovation ETF, the ARKK, up 57%; the IGV, the iShares Tech-Software ETF, up 52%; and the Philadelphia Semiconductor Index, up 185%.

Shares of Taiwan Semiconductor Manufacturing are down a couple points at the open, at $366.36 for the American Depository Receipts on the New York Stock Exchange, despite a strong report this morning, and an increased outlook for this year.

The proximate cause of the stock weakness, I would say, is the company merely reiterating its outlook from January to spend $52 billion to $56 billion in capital on plant and equipment this year, with CFO Wendell Huang saying the actual spending may be “towards the high end.”

Even though CEO C.C. Wei emphasized the positive take, that “supply is tight and demand continues to increase,” nevertheless, not increasing the actual dollar forecast of spend leaves some investors without what they would consider a sign of even greater confidence.

“This may have fallen short of more aggressive investor expectations” for capital spending, writes Krish Shankar of TD Cowen, a bull on the stock.